How Interest Rates Affect Business Valuations

Interest rates have a powerful ripple effect across the economy, influencing everything from consumer spending to the cost of capital. For business owners in Canada considering selling their business, understanding how interest rates affect their business is essential.

This post breaks down how interest rates impact valuation methods, what the recent rate cycle signals to buyers, and how owners can adapt using real-world strategies.

Overview

- Interest rates and business valuations have an inverse relationship: as rates fall, valuations generally rise.

- The Bank of Canada's policy rate, currently 2.75% as of July 2025↗, has been in an easing cycle since mid-2024, creating a more favourable valuation environment than the 5.00% peak seen in 2023.

- Discounted Cash Flow (DCF) and Capitalization of Earnings methods are highly sensitive to interest rates, which form the basis of their discount and capitalization rates.

- Owners can actively increase their company's value by de-risking operations and using creative deal structures, such as earn-outs and vendor financing.

What Interest Rates Mean for Valuations

At the core of business valuation is a tradeoff between risk and expected return. Buyers and investors assess a business’s future cash flows, then discount those future earnings back to today’s value based on how much risk they are taking on.

Interest rates play a central role in this calculation. They represent the "risk-free" benchmark, the return an investor could earn with minimal risk by placing funds in government bonds or similar instruments. All other investments, including private businesses, must offer a return that exceeds this baseline to justify the additional risk.

When interest rates are low, the risk-free benchmark is lower, meaning investors are more willing to pay a higher price today for future cash flows. This dynamic tends to support higher business valuations, especially for companies with stable, recurring earnings.

In contrast, when rates are high, investors and lenders demand steeper returns to compensate for increased opportunity cost and financing risk. This leads to higher discount rates in valuation models, which lower the present value of a business’s future earnings. For leveraged buyers, higher borrowing costs can also reduce the amount they are willing or able to pay, further reinforcing this downward price pressure.

This relationship is particularly important in industries where acquisitions are frequently financed with debt. As the cost of capital rises or falls, so too does the practical ceiling on what buyers can afford, even when the business’s fundamentals remain unchanged.

How Valuation Methods are Affected by Interest Rates

1. Discounted Cash Flow (DCF)

The DCF method projects a business’s expected future cash flows and discounts them to present value using a discount rate. This rate typically includes:

Risk-Free Rate (Rf): Often based on long-term Government of Canada bond yields, which are directly influenced by BoC policy.

Equity Risk Premium (ERP): The additional return investors require for taking on stock market risk over a risk-free investment.

Size Premium (SP): An added return for investing in small or private businesses, which are generally riskier.

Company-Specific Risk Premium (CSRP): A variable adjustment based on factors like customer concentration, owner dependence, and earnings volatility. This is the factor most within an owner’s control.

Example:

A business generating $500,000 per year in cash flow, discounted at 17%, is worth approximately $2.94 million. If the owner reduces operational risk (e.g., by diversifying clients or delegating operations), the CSRP may fall and the discount rate could drop to 12%. The same cash flow would then be worth about $4.17 million. Similar changes to the risk-free rate, equity risk premium, or size premium will force the value up or down.

2. Capitalization of Earnings

This method applies a capitalization rate to a single year of earnings. That cap rate is directly related to the discount rate, and therefore interest rates.

In a low-rate environment, cap rates decrease and valuations rise.

Example:

A business with $300,000 in Seller’s Discretionary Earnings (SDE), capitalized at 25% in a high-rate environment, is worth $1.2 million. If lower rates reduce the cap rate to 20%, the valuation rises to $1.5 million.

3. Market Multiples (EBITDA or SDE Multiples)

While market multiples are derived from actual transactions, they are still affected by interest rates indirectly:

- Buyers using debt can afford larger purchases when borrowing costs are lower

- Banks are more willing to lend, expanding the buyer pool

- As the cost of capital falls, multiples typically expand

The Canadian M&A market experienced renewed activity in late 2024 and into 2025, driven by these factors as well as the need for private equity firms to deploy accumulated capital.

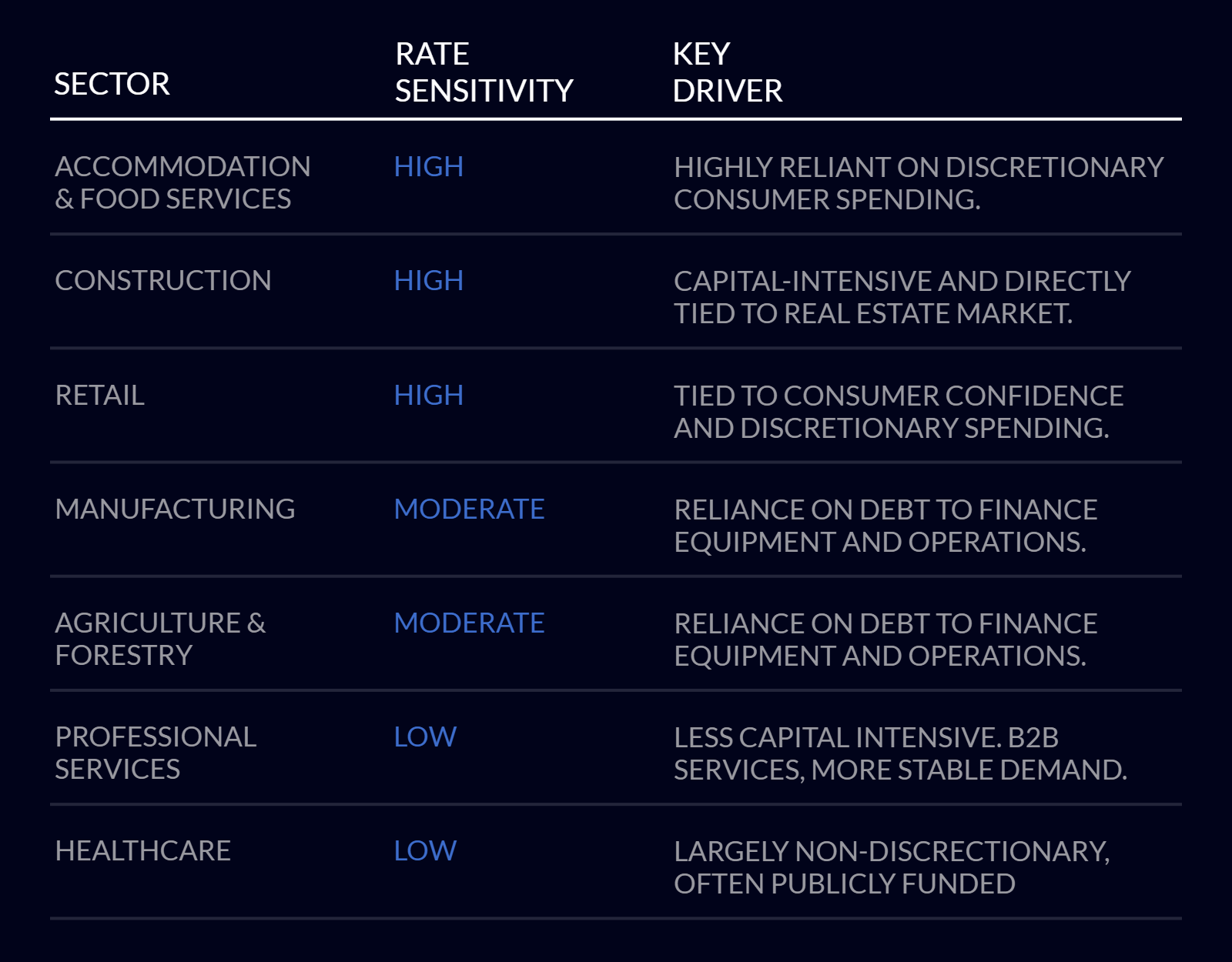

Industry Sensitivity to Interest Rates

Not all businesses are equally affected by interest rate changes. Industries that rely heavily on leverage or have long payback periods tend to be more sensitive.

High-growth technology and SaaS companies, even with minimal debt, are extremely interest rate sensitive. Their valuations depend on cash flows projected far into the future. When interest rates rise, those long-dated cash flows are more heavily discounted, significantly reducing present value.

What Business Owners Should Do

You can’t always time your business exit to align with ideal market conditions, but there are still effective strategies to help mitigate the impact of less favorable interest rate environments. Check out what increases a business’s valuation that most owners overlook↗ to uncover hidden value drivers in your business. A couple examples are provided below.

1. Reduce Company-Specific Risk

While you cannot control the Bank of Canada, you can reduce your business’s internal risk premium. Key strategies include:

- Diversify your customer base

- Develop a reliable, experienced management team

- Secure long-term contracts with customers and suppliers

- Document key processes and standard operating procedures (SOPs)

2. Use Flexible Deal Structures

Creative deal structures can help close valuation gaps when buyer and seller expectations diverge.

- Earn-Outs: A portion of the purchase price is paid after the sale based on performance targets (e.g., revenue or EBITDA). These allow sellers to benefit from future upside and reduce upfront risk for buyers. Earn-outs are used in approximately 28% of Canadian private M&A transactions.

- Vendor Take-Back (VTB) Financing: The seller lends the buyer part of the purchase price. VTBs can help deals close when traditional lenders are constrained and allow the seller to reach a higher price point while expanding the buyer pool.

Thinking About a Valuation?

At Flux Valuations, we specialize in Canadian small business valuations. Whether you're planning an exit, preparing for an internal buyout, or simply exploring your options, we can help you understand what your business is worth in today’s interest rate environment.

Start Your Valuation↗ or Contact Us↗ to learn more.

.jpg)